Merger and acquisition activity by JSE-listed companies over the first with three months of 2017 was, unsurprisingly and off a small base, on 2016 levels with 110 transactions announced balanced with 92 for Q1 2016 as being a pipeline of deals spilled over into 2017. The dip in transactions announced from the comparable 2016 period was largely a result of the upheaval due to Nenegate. The resultant political instability, regulatory uncertainty as well as the subsequent investment status downgrades have contributed to the latest slowdown in deals in South Africa. Total deal value with the quarter, excluding failed deals, was R78.4 billion.

In the unlisted space (companies unpublished over the JSE) M&A activity was up on the comparable period in 2016 with 60 deals recorded (50 deals in 2016) worth R14.8 billion. These deals 11 were private equity deals and 4 were BEE transactions. The best unlisted deal announced within the first quarter of the year was the $900 million (R11.7 billion) acquisition by Sinopec of a 75% stake in Chevron SA assets and 100% from the Botswana assets.

Investec Corporate Finance’s Eldad Friedman says the most recent cabinet reshuffle has a cloth affect investor confidence and, consequently, on deal flow. He said the results is often digested into your following: there was a lucid shift by investors towards companies with offshore investment components; institutions have shifted into stocks by using a heavy-weighting in international exposure. Institution, says Freidman, while being sensitive to those corporates new in offshore diversification, will are likely to favour those already offshore and; those companies that have sat undecided and hesitated before are actively pursuing offshore strategies. ??

Freidman says the slowdown inside buying local assets by foreigners is part due to a difficulty in understanding the political landscape, economy and how to make investment decisions in such a market. The upshot, according to him, is the fact that many deals are relegated towards back burner or focus has moved towards other jurisdictions in Africa C Africa has lost its preference because the launch pad into Africa. Foreign investors never have only become fewer but more selective in assets, avoiding heavy-regulated sectors like mining focusing rather on attractive assets in, such as, the meal sector which might be leveraged into Africa.

Other factors driving local M&A in the short term will be the really need to meet BEE ownership targets and multinationals who hold a portfolio of worldwide assets and who definitely are now reconsidering their South African investments which, given the investment conditions here, are negatively affecting their performance score cards. Purchasing of property portfolios by listed property funds remains a primary driver of activity for the JSE as is also forced offshore in the look for better yields.

These challenges, says Friedman, are further overlaid with currency risk. Concerns by rating agencies remain on account of poor medium-term growth prospects as a result of structural weaknesses, including rising rates, yet another deterioration inside investor climate in addition to a less supportive capital market environment, a concern provided that South Africa is tremendously influenced by external capital. 90 percent of debt is local currency denominated. On top of that the possibilities of further rises in the government debt-to-GDP ratio is implied because of the low-growth environment.

David Gewer, director at Werksmans Attorneys, says investor nervousness has affected local and foreign investors while in the unlisted space. According to while we have witnessed disposals by a few multinationals in private companies there has also been acquisitions by multinationals. A noticeable trend within the last few year may be the rise in distressed transactions, particularly mining. Companies operating rescue and undergoing restructuring, offer opportunity to buyers trying to acquire assets at favourable prices. Foreign investors, Gewer says, ought to chase yields there will always be interest, there’ll be ebbs and flows with respect to the cycle.

Interestingly M&A activity for the lower value level (between R20m and R200m) has throughout the last two years been invulnerable to the political volatility says Chris Staines, head of corporate finance at Grant Thornton in Cape Town. These transactions according to are characterised usually by small family owned businesses.

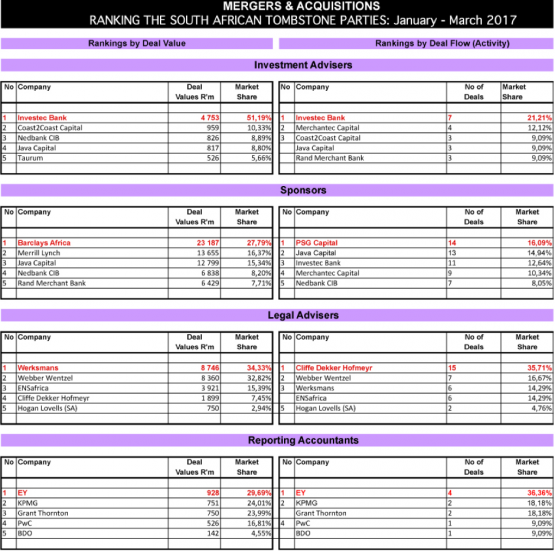

Analysis and rankings by DealMakers of M&A activity of each and every South African advisory firm (in connection with JSE-listed companies) is reflected below. The effects will be in respect of your first quarter of 2017.

General Corporate Finance activities on the JSE-listed companies still give a solid underpin for the advisory firms. In Q1 capital raised by companies through the issue of shares totalled R22 billion which often rights issues included R13 billion, the greatest ones was the R9 billion raised by Life Healthcare. Seven initial public offerings (IPOs) were launched just before listings for the JSE, comprising R4 billion; Long4Life taken into account half this value.

Advisory firm rankings while in the activities of general corporate finance for any first quarter of 2017 are as follows:

Looking ahead, Freidman says deal activity will keep, albeit on a slow pace, with institutions having to deploy cash; the main element theme could be to buy companies with international connections in lieu of those dependent solely on South African generated revenue.